Profitability analysis enables the evaluation of market segments (products, customers, orders, or any combination of these, or strategic business units, such as sales organizations or business areas) concerning the company’s profit or contribution margin.

The system aims to provide all relevant segments and departments with information that supports internal accounting and decision-making.

There are two forms of profitability analysis supported, and both types can be used simultaneously:

- Costing-based profitability analysis: This groups cost and revenues according to value fields and costing-based valuation approaches, whereas both can be defined, always assuring access to a complete, short-term profitability report.

- Margin analysis (formerly called account-based profitability analysis): This is organized in accounts and uses an account-based valuation approach. The difference in this form is its use of cost and revenue elements, providing a profitability report permanently reconciled with financial accounting.

RAR integrates with profitability analysis using the sales and distribution entry to profitability analysis, as it behaves like sales and distribution billing documents. Therefore, the actual value flow is defined by assigning condition types to value fields, similar to sales and distribution billing documents.

In the IMG, go to menu path Controlling > Profitability Analysis > Flow of Actual Values > Transfer of Billing Documents > Assign Value Fields > Maintain Assignment of SD Conditions to CO-PA Value Field.

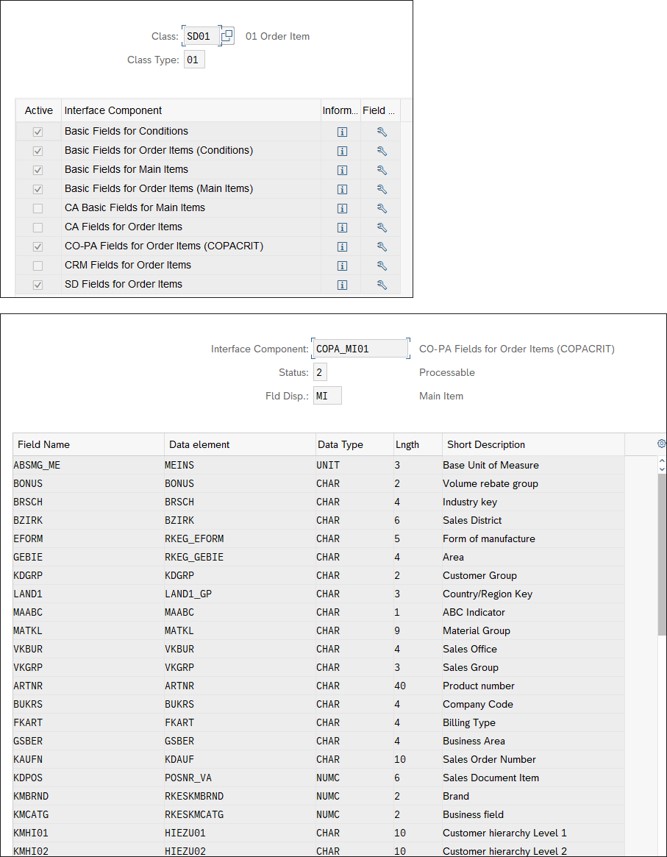

Profitability analysis integration with RAR is handled mainly as controlling setup. If profitability analysis is active, the interface component profitability analysis characteristics are by default activated in the configuration of RAI classes for order items (RAI class type 01; see top screen in the figure below). The activation of this interface component can’t be deselected. The interface component contains all the fields of structure COPACRIT, as shown in the bottom screen in the figure. Fields from structure COPACRIT are transferred to the profitability segment number by transforming raw items into processable items.

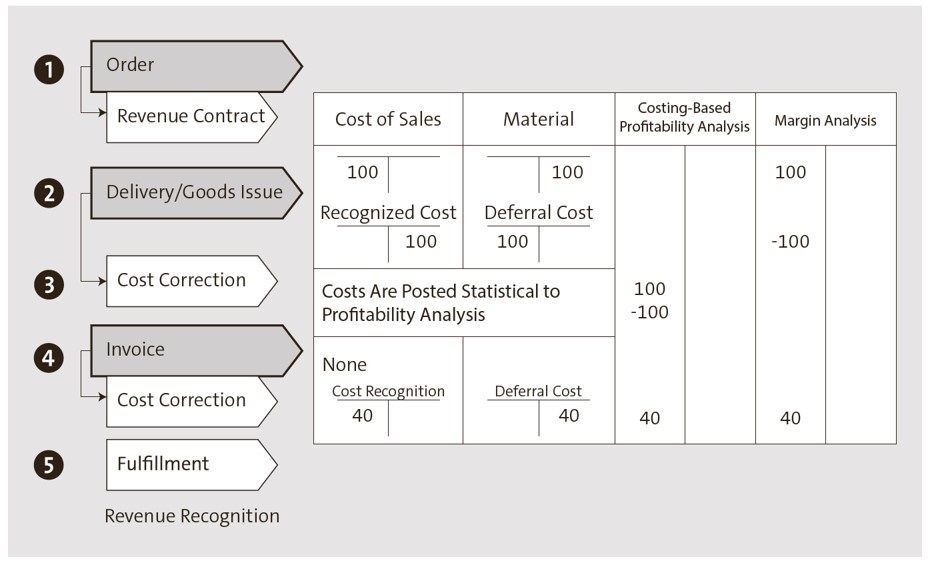

The next figure shows different treatment of postings in costing-based profitability analysis and margin analysis. The first difference is that at the moment of goods issue, COGS are posted in margin analysis, whereas in costing-based profitability analysis, you need to wait for the invoice when COGS are getting posted statistically. If you add RAR cost corrections into the equation, reversal of COGS will be posted in margin analysis, but not in costing-based profitability analysis. At the end, the result of both approaches is the same, but with different postings in different steps.

The following steps describe a typical business process for cost recognition:

- The order includes the COGS in a condition. This is the main condition where subsequent accounts are derived from, and there can only be one main cost condition. Cost conditions other than the main cost condition are ignored with the exception of capitalized cost. The order creates a revenue accounting contract. There are no financial accounting postings in this step. For external components, the account assignment is done in BRFplus.

- The goods issue or delivery triggers a financial accounting posting with cost of sales (CoS) in debit and material in credit. Margin analysis is updated if active.

- The goods issue forwards the COGS to RAR. A correction posting is created with the posting run, which reverses the financial accounting and profitability analysis posting of step 2.

- The invoice updates the costing-based profitability analysis with COGS. As the invoice is forwarded to RAR, a reverse posting is created with the posting run.

- The fulfillment posts revenues and costs according to the cost matching principle. The costs are posted to financial accounting, costing-based profitability analysis, and margin analysis. In the example, 40% of the revenues have been fulfilled despite the delivery. Therefore, 40% of the CoS are posted to financial accounting and profitability analysis.

Cost is posted to profitability analysis when its corresponding revenue is posted. You need to set up the condition type for goods issue (e.g., VPRS). Ensure that the cost element of the general ledger account derived from the condition type has cost element category 12 (sales deductions).

In costing-based profitability analysis, if you’re using VPRS as the cost condition type, Transfer +/- must not be set. The cost condition needs to be defined this way because otherwise, the profitability analysis component would raise an error message if it gets positive and negative values for the same profitability segment during the posting run.

As RAR delivers positive and negative values to profitability analysis, the Transfer +/- indicator must be set for assigning the condition type to the value field, including the following settings:

- For the CoS (condition category G, e.g., VPRS), the Transfer +/- flag must not be set.

- In the right of returns (RORs), assign value fields for the ROR cost, and revenue adjustments are needed.

Editor’s note: This post has been adapted from a section of the book Revenue Accounting and Reporting with SAP S/4HANA by Sreten Milosavljević and Swayam Prabha Shankara.

Comments